The initial Q2 GDP estimate of 2.8% came as a surprise, exceeding the consensus view of +2.0%. Despite this positive growth, the equity markets responded tepidly, with selling pressure leading to a decline at the end of the day. The positive aspects of GDP growth included unwanted inventory accumulation and government spending growth, as well as a decrease in the savings rate, which was offset by rising credit card balances and high delinquencies. Without certain factors, GDP growth would have been closer to +0.5%.

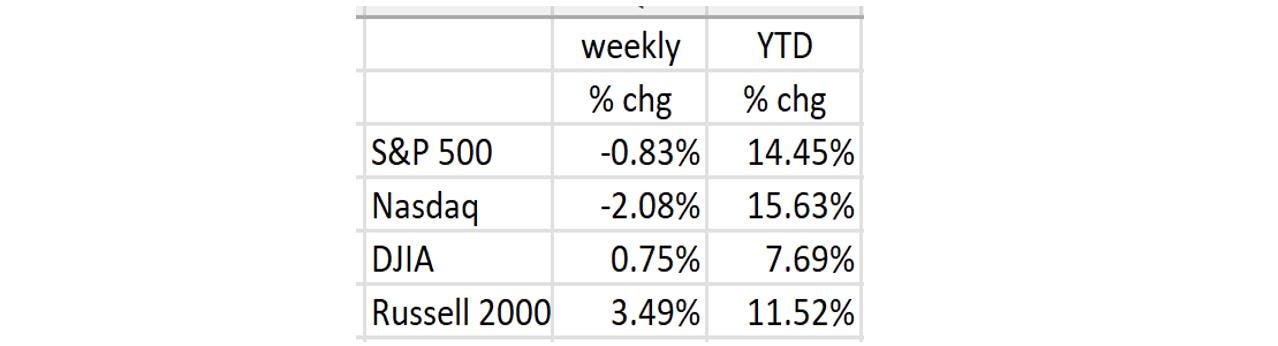

The Personal Consumption Expenditure Index (PCE), a key inflation gauge, showed a modest increase of +0.1% for June, lowering the year-over-year inflation rate to 2.5%. This subdued inflation rate led to a market rally, with the DJIA, Nasdaq, S&P500, and Russell 2000 all posting gains on Friday. However, the gains were not enough to offset the negative performance of the S&P 500 and Nasdaq for the week.

The small cap Russell 2000 index saw a significant rise following expectations of Fed rate reductions, with market sentiment shifting away from large cap companies. The Magnificent 7 companies experienced price declines despite the market rally. The expected rate cuts by the Fed are anticipated to ease the leverage burden on smaller companies and support their rally.

Incoming data suggests economic softness, with negative readings in various economic indicators such as the Chicago Fed’s National Activity Index and the Philadelphia Fed’s Non-Manufacturing Index. Existing home sales and new home sales have also declined, with high levels of unsold inventory in the housing market. Inflation is showing signs of decline, with falling prices in raw materials and the possibility of deflation in the near future.

Corporate performance has been impacted by economic softness, with companies like UPS, FedEx, Nestle, Southwest Airlines, American Airlines, Tesla, Comcast, and AT&T reporting lower earnings and revenues. The Fed’s restrictive policy is affecting various sectors, including the housing market, corporate profits, and commercial real estate (CRE). The CRE market continues to deteriorate, with reports of large foreclosures, raising concerns about the quality of loan portfolios among U.S. lenders.

Overall, while Q2 GDP growth exceeded expectations, several unsustainable factors contributed to this growth. Challenges in the housing market, corporate performance, and the CRE market, combined with indications of economic softness, suggest that the economy may face difficulties in the coming months. The prospect of lower rates and easing leverage for small businesses may support a shift in investor sentiment towards small cap stocks, while inflation appears to be on the decline.