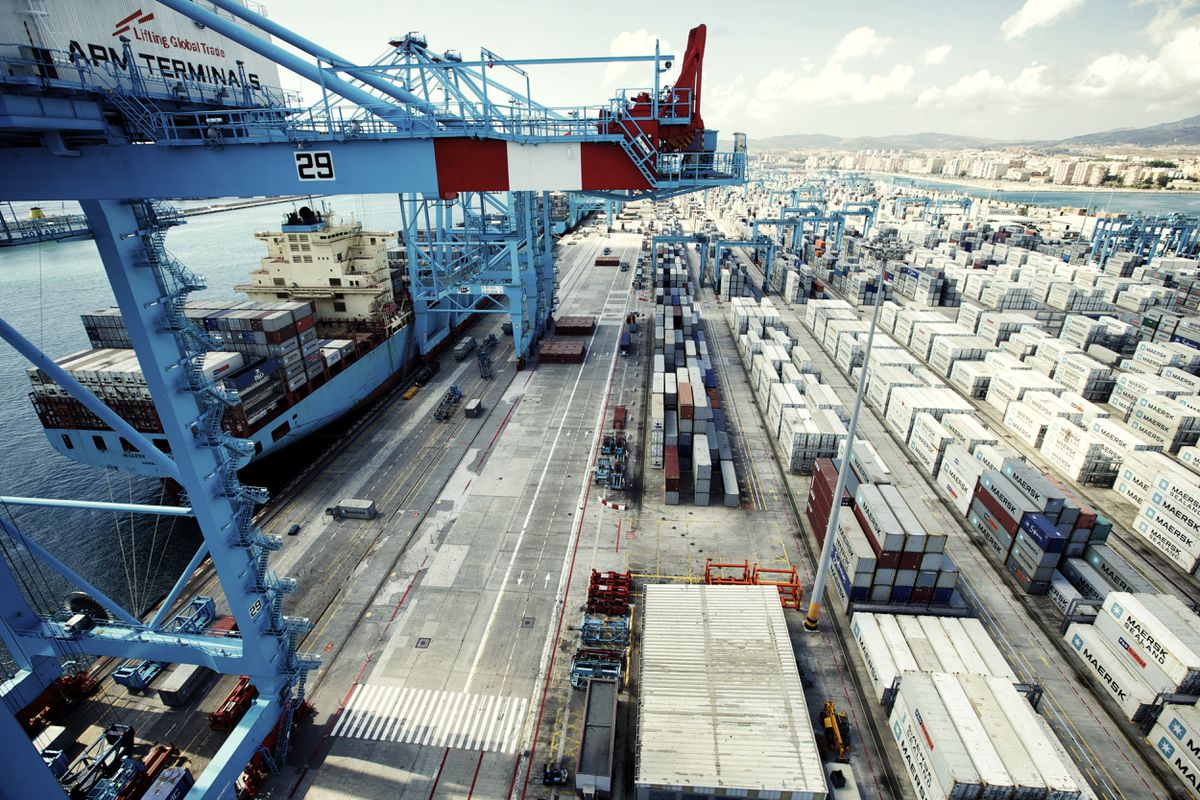

The geopolitical tensions in the Middle East and their military escalation, in addition to the dramatic consequences for the population, are having a surprising impact on the Spanish economy. On one hand, the bulk of the productive fabric is being affected, just like in the rest of Europe, by the climate of uncertainty that hampers confidence and makes it difficult for investment to take off, which is key to the continuation of the expansion cycle. The rise in oil prices and maritime transportation passing through the regions near the conflict complicates the path of disinflation, while eroding purchasing power. However, global turbulence is accompanied by huge inflows of foreign investment, attracted by the low labor and energy costs in comparison to other economies in our environment.

Recent announcements of positions in the technology, energy, and automotive sectors are part of a trend due to the significant amount of foreign capital being invested in Spanish companies, especially in large corporations. In the last two years, foreign direct investment (excluding speculative financial capital) reached an average of 2.9% of the GDP, a much higher figure than observed in other major EU partners. Additionally, Spain is a net importer of foreign capital, unlike Germany, for example, which exports a large part of its savings to equip companies in other countries. Investors reason globally, and in that comparison, Spain is not doing badly as uncertainties are similar across the continent, but Spain is far from the main conflict zones and production costs are favorable.

The dual nature of the investment climate, with large corporations attracting foreign capital while small and medium-sized enterprises struggle due to local conditions and lingering trauma from the financial crisis, is important for economic policy. The deficit in investment mainly affects small and medium-sized enterprises, rather than corporations capable of attracting foreign capital. The recently announced initiative to co-finance companies led by Cofides is a step in the right direction by aiming to bring resources to strategic sectors, potentially benefiting medium-sized companies. However, the funding volume of this initiative (2 billion euros, financed with Next Generation loans) seems insufficient to address the investment drought. More decisive would be the financial union proposed by Brussels to facilitate savings mobility to boost the European economy, but the project faces opposition from countries resistant to regulatory and fiscal harmonization.

A medium-term budgetary path would be another lever to unlock investment among companies most affected by uncertainties and unable to access international financing due to their size. The General State Budgets are the main instrument of economic policy, and public action coherence depends on them. Paradoxically, global volatility is more harmful to Spanish SMEs than to international investors who continue to bet on our productive fabric. This dichotomy is likely to increase as the conflict in the Middle East persists or spreads. Foreign capital invested in Spanish companies last year reached 33 billion euros, with investors from the EU, US, and UK contributing most of the funds, while Gulf monarchies and China also play a role, albeit smaller. The presence of China is rapidly growing in the Spanish market.