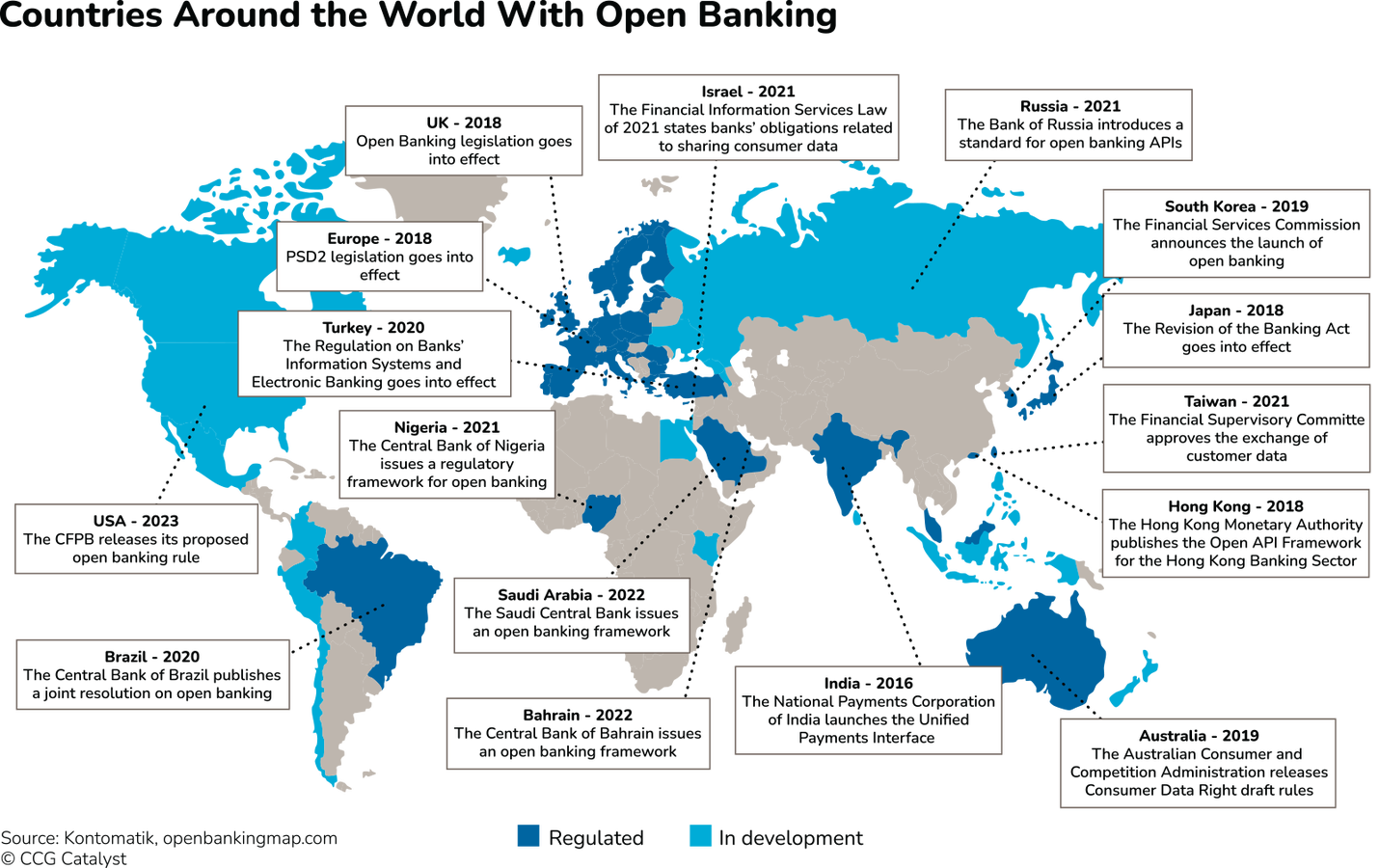

The Consumer Financial Protection Bureau is set to finalize its open banking rule this fall, requiring financial institutions to provide access to customers’ financial data to third parties upon request. This will include data from checking, savings, credit card accounts, prepaid cards, and digital wallets. The real challenge for financial institutions lies in figuring out how to comply with this rule, especially considering the existing legacy infrastructure that many institutions have in place.

According to data from Forbes Insights and Thought Machine, a majority of bankers find legacy infrastructure to be a major challenge when it comes to integrating and sharing data. The key to open banking lies in the ability to share data externally through standardized application programming interfaces (APIs). As a result, financial institutions need to start thinking about how to prepare their infrastructure to support the data-sharing interfaces required by open banking. This may involve seeking help and knowledge to inform their strategy, especially for smaller institutions that do not have the necessary foundations in place.

There are three primary avenues that financial institutions can explore to prepare for open banking compliance. They can turn to bank technology and digital banking providers, such as FIS, Fiserv, JHA, Q2, and Alkami, who are aware of the role they will play in helping their clients comply with the CFPB’s rule. Third-party aggregators like Plaid or Tink are also working to get ahead of the rule by partnering with FIs and other technology providers. In-house developers may also play a role in building the infrastructure needed for open banking compliance, especially for institutions that are forward-thinking and want to plan beyond mere compliance.

Financial institutions should be looking to consult a range of experts as they develop their open banking strategies. While some institutions may focus solely on achieving compliance, others may be more forward-thinking and consider additional use cases beyond the scope of the CFPB’s rule. By seeking knowledge and getting informed about the possibilities of open banking, FIs can begin to develop strategies that work for their specific needs and goals. Compliance is just the starting point, and the most successful institutions will look for ways to differentiate themselves in the open banking landscape.

It is important to note that the CFPB’s rule only covers certain types of data, leaving many other potential use cases to be explored. While basic compliance is essential, the most successful financial institutions will go a step further and seek ways to differentiate themselves in the open banking space. Whether an institution is focused solely on compliance or thinking ahead to future opportunities, understanding what open banking entails and how to navigate this new landscape is crucial for long-term success. By taking a proactive approach and seeking out the necessary expertise, FIs can position themselves for success in the evolving world of open banking.