Dealing with the loss of a loved one is emotionally challenging and can be compounded by the legal complexities of settling their estate. In some cases, the probate process can be overwhelming due to strict procedural requirements and a lengthy duration. This article outlines the steps involved in estate settlement, offering insights on preemptive measures to avoid probate delays and special considerations for estates that include unique assets such as artwork, vacation properties, or family-owned businesses.

The initial steps of settling an estate involve immediate administrative tasks and beginning the probate process. Families must handle duties such as organizing the funeral, obtaining crucial documents like the will and death certificates, and initiating probate proceedings. Concurrently, the probate process kicks off with the preparation and submission of necessary documents to the Probate Court, including the petition for probate and other initial paperwork. The authenticity of the will is confirmed, notices are sent to concerned parties, and appointments are arranged as needed.

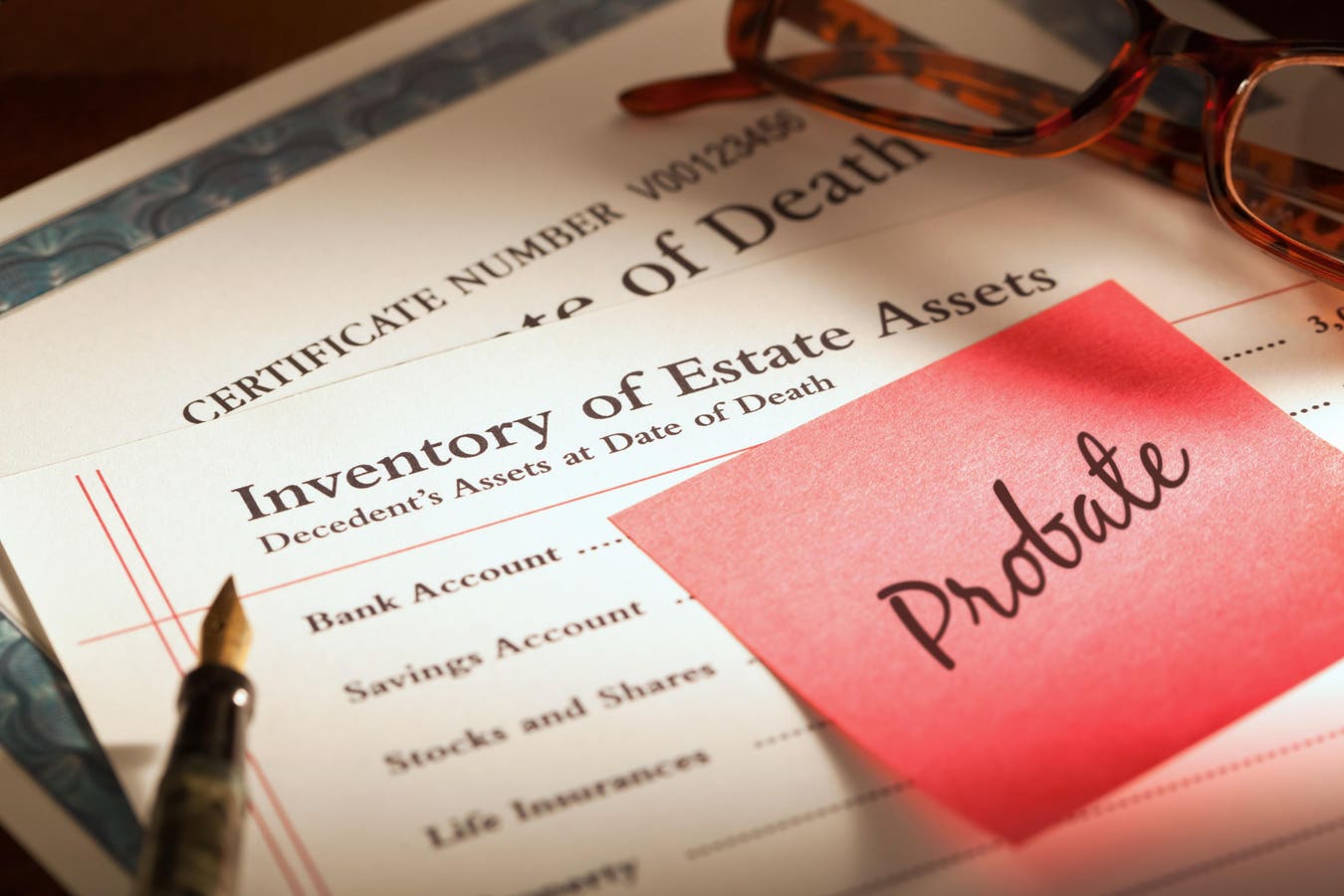

In the subsequent months, the executor or administrator of the estate must manage assets, assess real estate values, and handle tax obligations. This includes selecting the estate’s fiscal year, obtaining a tax identification number, and managing the deceased’s final income tax returns. As the process progresses, the executor must consider filing an estate tax return if necessary. Additionally, steps are taken to disclaim interests, obtain waivers, distribute specific bequests, and possibly sell property to benefit the estate.

As the estate settlement process continues into the mid to late phases, the executor focuses on distributing assets, deciding on the sale of property, and resolving any outstanding financial matters. The final year is dedicated to finalizing distributions to heirs, allocating assets to trusts as specified in the will, and settling all financial obligations. Beneficiaries are often surprised by the length of time it takes to settle an estate and receive their bequests.

Even after the estate is closed, ongoing responsibilities include monitoring unclaimed property in the deceased’s name. Executors must collaborate with legal professionals throughout the process to meet deadlines, fulfill legal obligations, and make informed decisions. To streamline the estate settlement process and reduce the financial and emotional burden on grieving families, proactive measures such as thorough estate planning, utilizing revocable living trusts, and updating estate documents regularly are recommended.

Dealing with unique assets in an estate, such as artwork, collectibles, family businesses, or vacation properties, introduces additional complexities. Valuation challenges, liquidity issues, tax considerations, legal and regulatory hurdles, emotional dynamics, and maintenance demands all need to be carefully navigated. Strategic estate planning, including establishing specific trusts, obtaining professional valuations, and fostering transparent communication with potential heirs, can help mitigate these challenges and ensure a smoother transition of assets.

Proactive and strategic estate planning is crucial for safeguarding asset value, minimizing family discord, and ensuring a seamless transfer of assets to the next generation. Consulting with estate planning professionals can help tailor a plan to meet individual needs and circumstances, providing peace of mind for both the estate owner and their loved ones. By taking the necessary steps now to address estate planning, individuals can secure their legacy and protect their assets for the future.